The best travel insurance policies and providers

It's easy to dismiss the value of travel insurance until you need it.

Many travelers have strong opinions about whether you should buy travel insurance . However, the purpose of this post isn't to determine whether it's worth investing in. Instead, it compares some of the top travel insurance providers and policies so you can determine which travel insurance option is best for you.

Of course, as the coronavirus remains an ongoing concern, it's important to understand whether travel insurance covers pandemics. Some policies will cover you if you're diagnosed with COVID-19 and have proof of illness from a doctor. Others will take coverage a step further, covering additional types of pandemic-related expenses and cancellations.

Know, though, that every policy will have exclusions and restrictions that may limit coverage. For example, fear of travel is generally not a covered reason for invoking trip cancellation or interruption coverage, while specific stipulations may apply to elevated travel warnings from the Centers for Disease Control and Prevention.

Interested in travel insurance? Visit InsureMyTrip.com to shop for plans that may fit your travel needs.

So, before buying a specific policy, you must understand the full terms and any special notices the insurer has about COVID-19. You may even want to buy the optional cancel for any reason add-on that's available for some comprehensive policies. While you'll pay more for that protection, it allows you to cancel your trip for any reason and still get some of your costs back. Note that this benefit is time-sensitive and has other eligibility requirements, so not all travelers will qualify.

In this guide, we'll review several policies from top travel insurance providers so you have a better understanding of your options before picking the policy and provider that best address your wants and needs.

The best travel insurance providers

To put together this list of the best travel insurance providers, a number of details were considered: favorable ratings from TPG Lounge members, the availability of details about policies and the claims process online, positive online ratings and the ability to purchase policies in most U.S. states. You can also search for options from these (and other) providers through an insurance comparison site like InsureMyTrip .

When comparing insurance providers, I priced out a single-trip policy for each provider for a $2,000, one-week vacation to Istanbul . I used my actual age and state of residence when obtaining quotes. As a result, you may see a different price — or even additional policies due to regulations for travel insurance varying from state to state — when getting a quote.

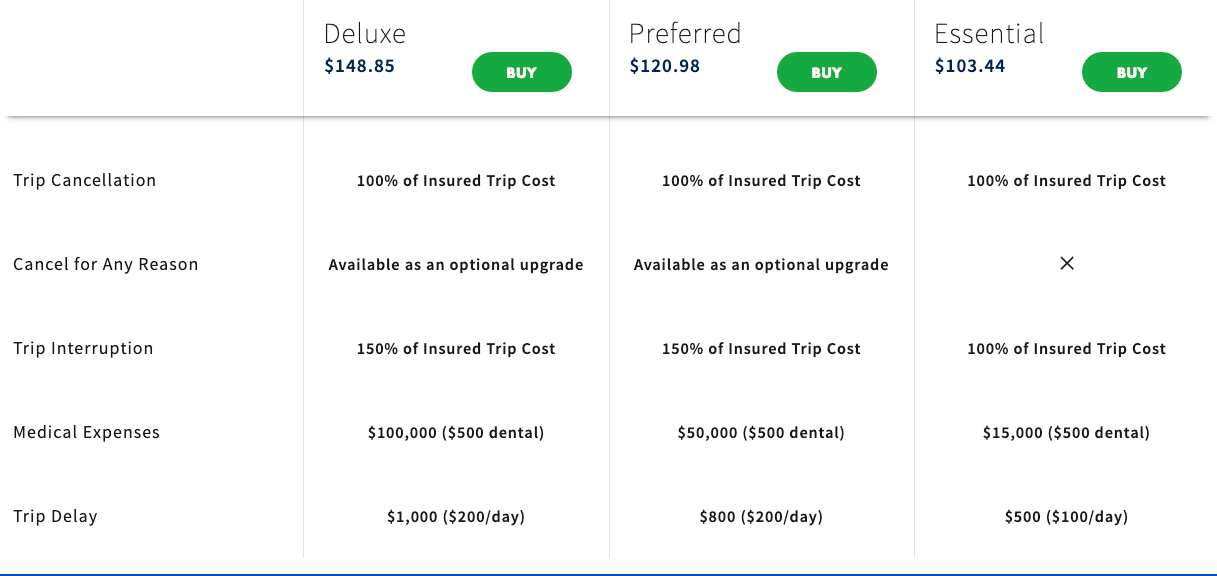

AIG Travel Guard

AIG Travel Guard receives many positive reviews from readers in the TPG Lounge who have filed claims with the company. AIG offers three plans online, which you can compare side by side, and the ability to examine sample policies. Here are three plans for my sample trip to Turkey.

AIG Travel Guard also offers an annual travel plan. This plan is priced at $259 per year for one Florida resident.

Additionally, AIG Travel Guard offers several other policies, including a single-trip policy without trip cancellation protection . See AIG Travel Guard's COVID-19 notification and COVID-19 advisory for current details regarding COVID-19 coverage.

Preexisting conditions

Typically, AIG Travel Guard wouldn't cover you for any loss or expense due to a preexisting medical condition that existed within 180 days of the coverage effective date. However, AIG Travel Guard may waive the preexisting medical condition exclusion on some plans if you meet the following conditions:

- You purchase the plan within 15 days of your initial trip payment.

- The amount of coverage you purchase equals all trip costs at the time of purchase. You must update your coverage to insure the costs of any subsequent arrangements that you add to your trip within 15 days of paying the travel supplier for these additional arrangements.

- You must be medically able to travel when you purchase your plan.

Standout features

- The Deluxe and Preferred plans allow you to purchase an upgrade that lets you cancel your trip for any reason. However, reimbursement under this coverage will not exceed 50% or 75% of your covered trip cost.

- You can include one child (age 17 and younger) with each paying adult for no additional cost on most single-trip plans.

- Other optional upgrades, including an adventure sports bundle, a baggage bundle, an inconvenience bundle, a pet bundle, a security bundle and a wedding bundle, are available on some policies. So, an AIG Travel Guard plan may be a good choice if you know you want extra coverage in specific areas.

Purchase your policy here: AIG Travel Guard .

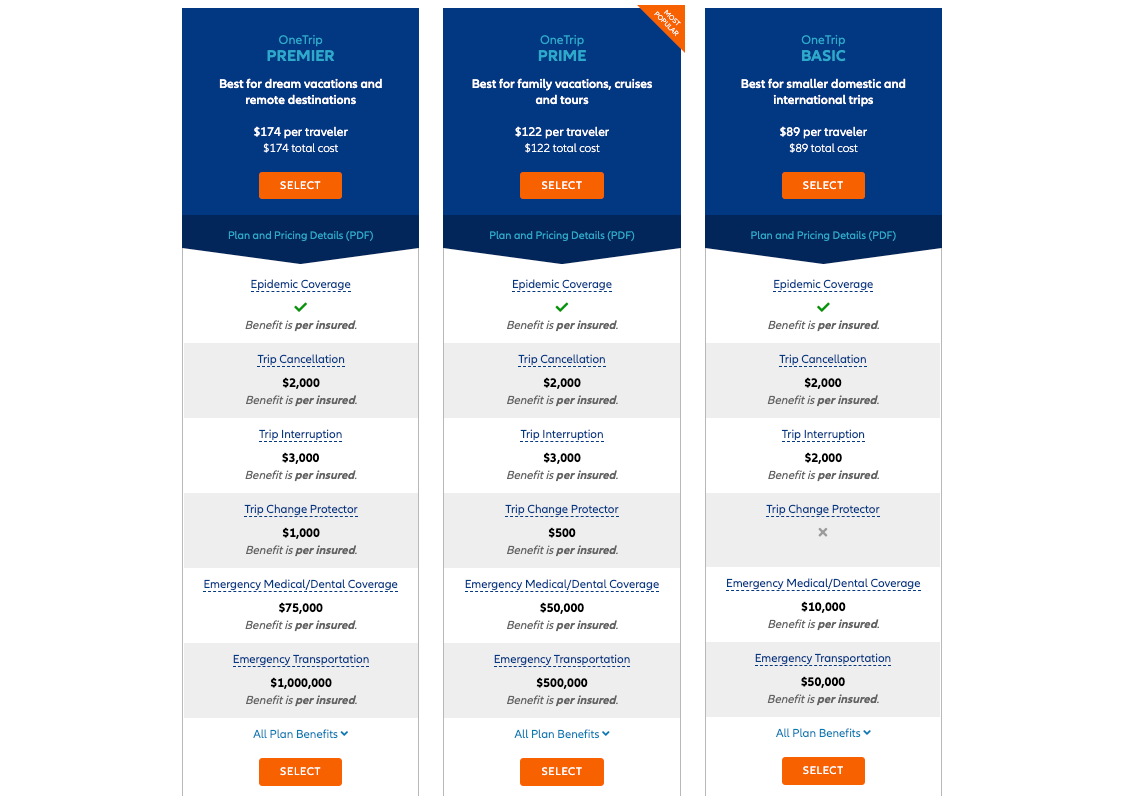

Allianz Travel Insurance

Allianz is one of the most highly regarded providers in the TPG Lounge, and many readers found the claim process reasonable. Allianz offers many plans, including the following single-trip plans for my sample trip to Turkey.

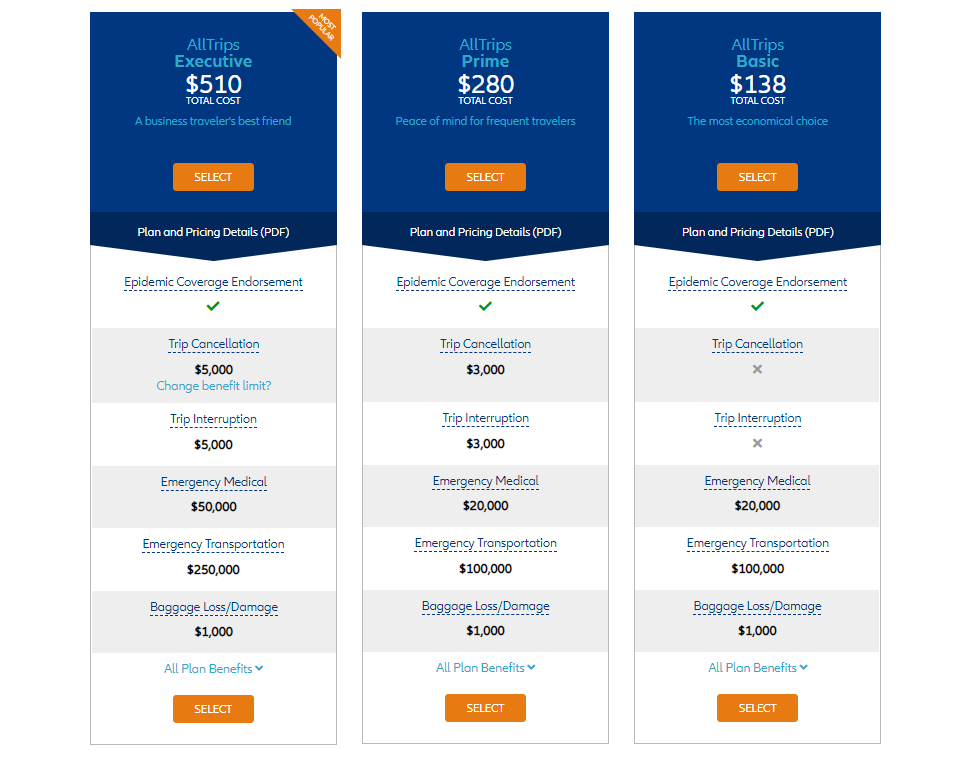

If you travel frequently, it may make sense to purchase an annual multi-trip policy. For this plan, all of the maximum coverage amounts in the table below are per trip (except for the trip cancellation and trip interruption amounts, which are an aggregate limit per policy). Trips typically must last no more than 45 days, although some plans may cover trips of up to 90 days.

See Allianz's coverage alert for current information on COVID-19 coverage.

Most Allianz travel insurance plans may cover preexisting medical conditions if you meet particular requirements. For the OneTrip Premier, Prime and Basic plans, the requirements are as follows:

- You purchased the policy within 14 days of the date of the first trip payment or deposit.

- You were a U.S. resident when you purchased the policy.

- You were medically able to travel when you purchased the policy.

- On the policy purchase date, you insured the total, nonrefundable cost of your trip (including arrangements that will become nonrefundable or subject to cancellation penalties before your departure date). If you incur additional nonrefundable trip expenses after purchasing this policy, you must insure them within 14 days of their purchase.

- Allianz offers reasonably priced annual policies for independent travelers and families who take multiple trips lasting up to 45 days (or 90 days for select plans) per year.

- Some Allianz plans provide the option of receiving a flat reimbursement amount without receipts for trip delay and baggage delay claims. Of course, you can also submit receipts to get up to the maximum refund.

- For emergency transportation coverage, you or someone on your behalf must contact Allianz, and Allianz must then make all transportation arrangements in advance. However, most Allianz policies provide an option if you cannot contact the company: Allianz will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Allianz Travel Insurance .

American Express Travel Insurance

American Express Travel Insurance offers four different package plans and a build-your-own coverage option. You don't have to be an American Express cardholder to purchase this insurance. Here are the four package options for my sample weeklong trip to Turkey. Unlike some other providers, Amex won't ask for your travel destination on the initial quote (but will when you purchase the plan).

Amex's build-your-own coverage plan is unique because you can purchase just the coverage you need. For most types of protection, you can even select the coverage amount that works best for you.

The prices for the packages and the build-your-own plan don't increase for longer trips — as long as the trip cost remains constant. However, the emergency medical and dental benefit is only available for your first 60 days of travel.

Typically, Amex won't cover any loss you incur because of a preexisting medical condition that existed within 90 days of the coverage effective date. However, Amex may waive its preexisting-condition exclusion if you meet both of the following requirements:

- You must be medically able to travel at the time you pay the policy premium.

- You pay the policy premium within 14 days of making the first covered trip deposit.

- Amex's build-your-own coverage option allows you to only purchase — and pay for — the coverage you need.

- Coverage on long trips doesn't cost more than coverage for short trips, making this policy ideal for extended getaways. However, the emergency medical and dental benefit only covers your first 60 days of travel.

- American Express Travel Insurance can protect travel expenses you purchase with Amex Membership Rewards points in the Pay with Points program (as well as travel expenses bought with cash, debit or credit). However, travel expenses bought with other types of points and miles aren't covered.

Purchase your policy here: American Express Travel Insurance .

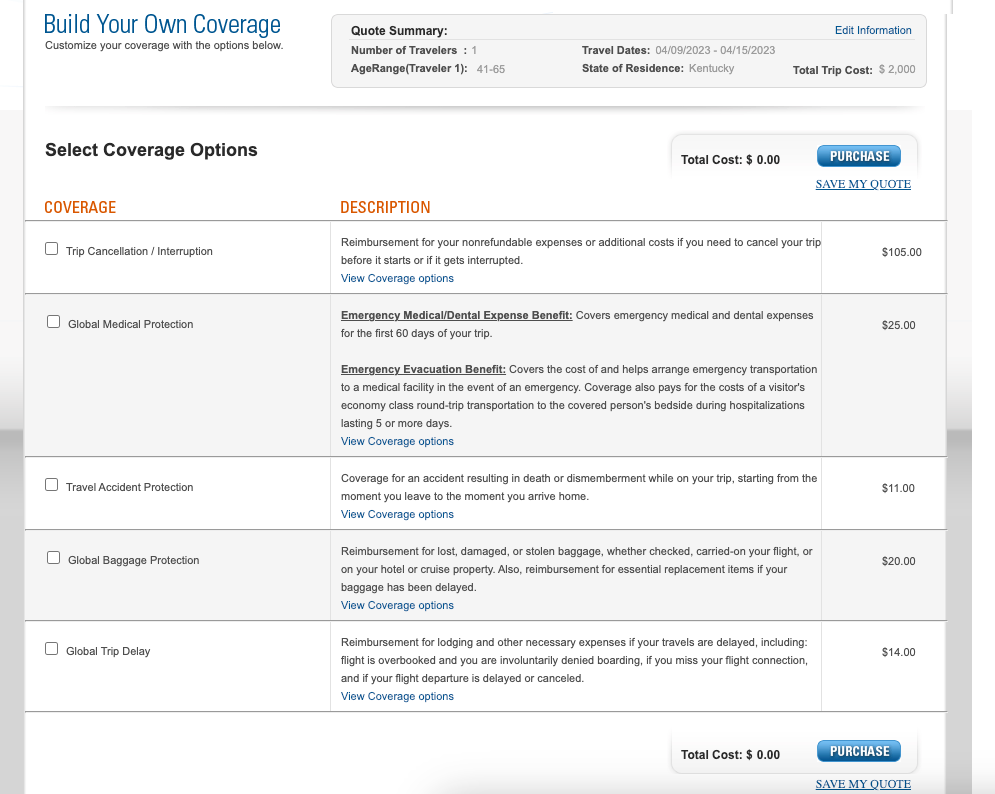

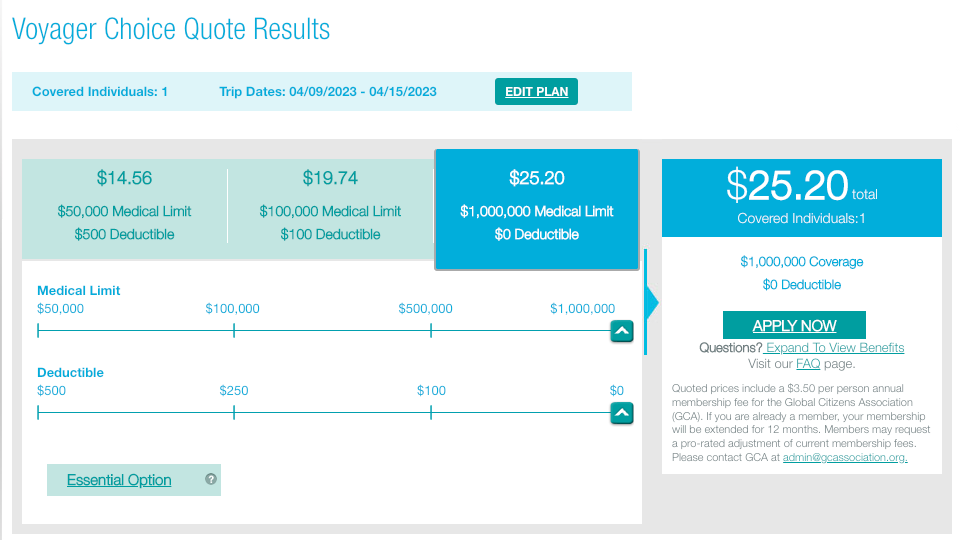

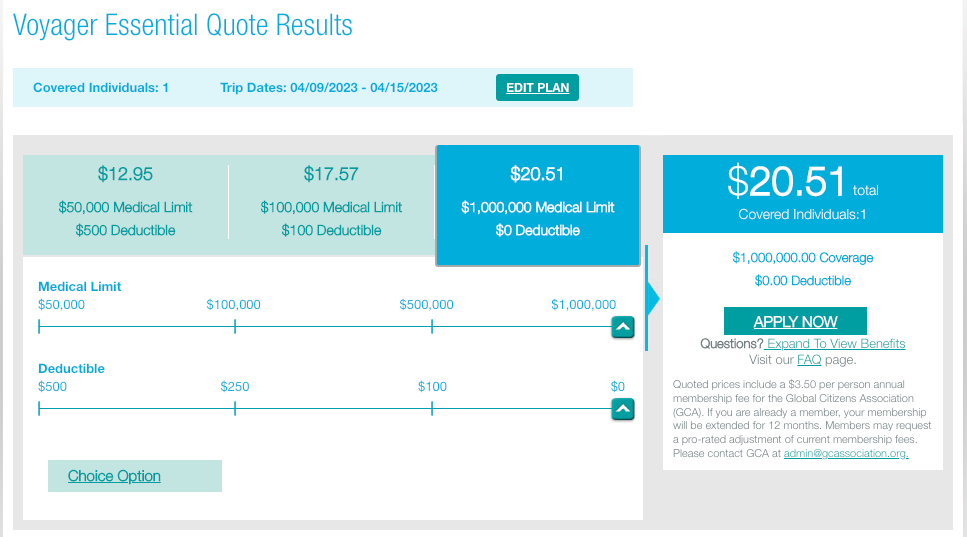

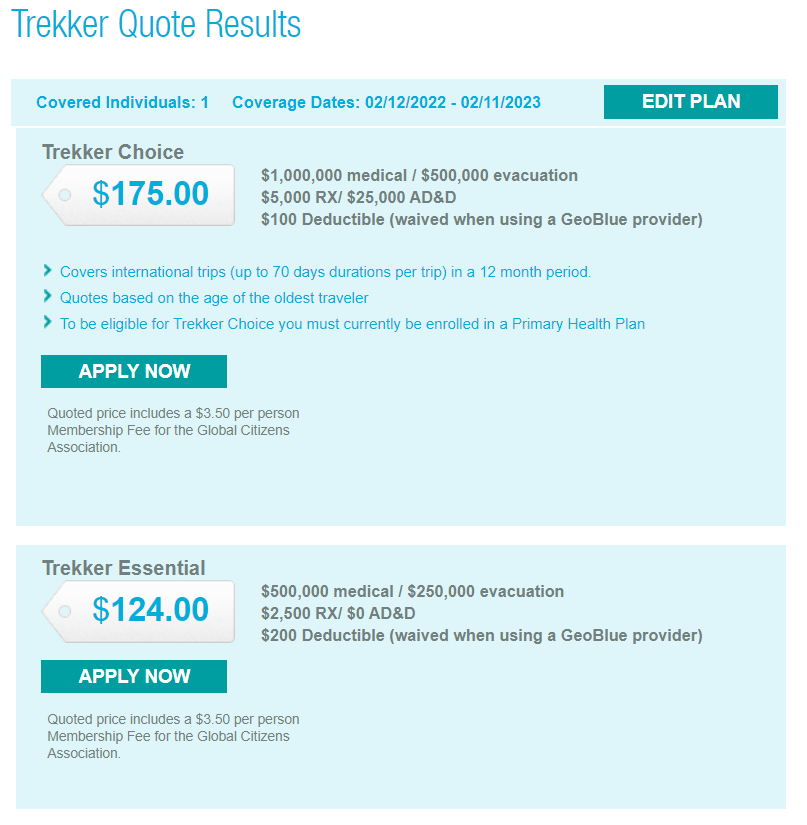

GeoBlue is different from most other providers described in this piece because it only provides medical coverage while you're traveling internationally and does not offer benefits to protect the cost of your trip. There are many different policies. Some require you to have primary health insurance in the U.S. (although it doesn't need to be provided by Blue Cross Blue Shield), but all of them only offer coverage while traveling outside the U.S.

Two single-trip plans are available if you're traveling for six months or less. The Voyager Choice policy provides coverage (including medical services and medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger and already have a U.S. health insurance policy.

The Voyager Essential policy provides coverage (including medical evacuation for a sudden recurrence of a preexisting condition) for trips outside the U.S. to travelers who are 95 or younger, regardless of whether they have primary health insurance.

In addition to these options, two multi-trip plans cover trips of up to 70 days each for one year. Both policies provide coverage (including medical services and medical evacuation for preexisting conditions) to travelers with primary health insurance.

Be sure to check out GeoBlue's COVID-19 notices before buying a plan.

Most GeoBlue policies explicitly cover sudden recurrences of preexisting conditions for medical services and medical evacuation.

- GeoBlue can be an excellent option if you're mainly concerned about the medical side of travel insurance.

- GeoBlue provides single-trip, multi-trip and long-term medical travel insurance policies for many different types of travel.

Purchase your policy here: GeoBlue .

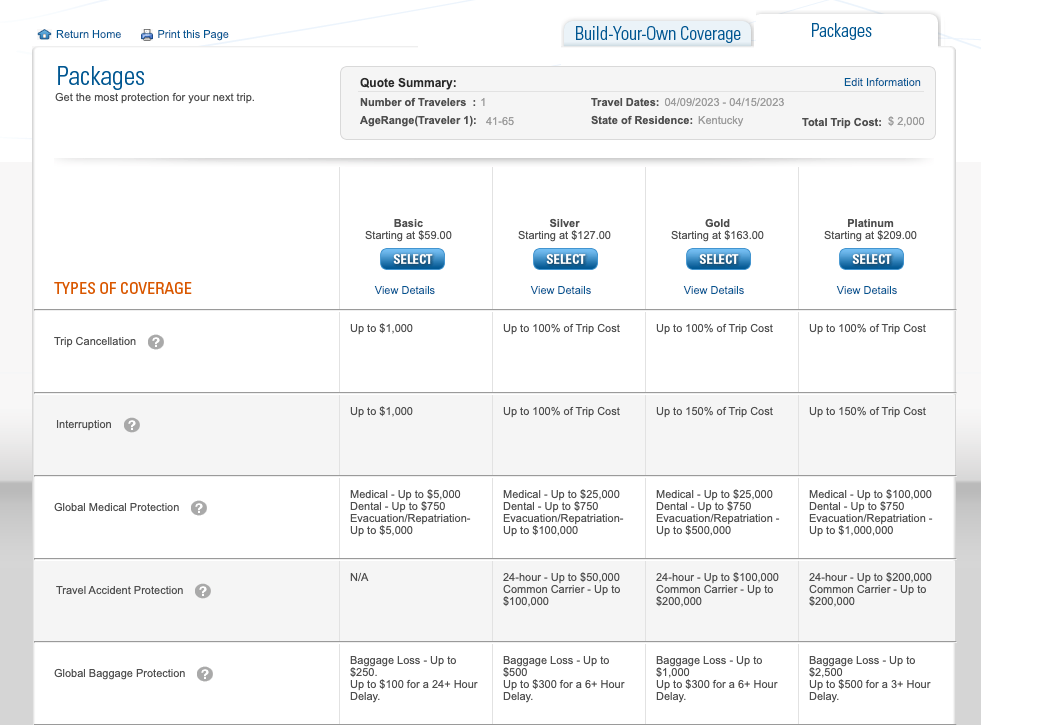

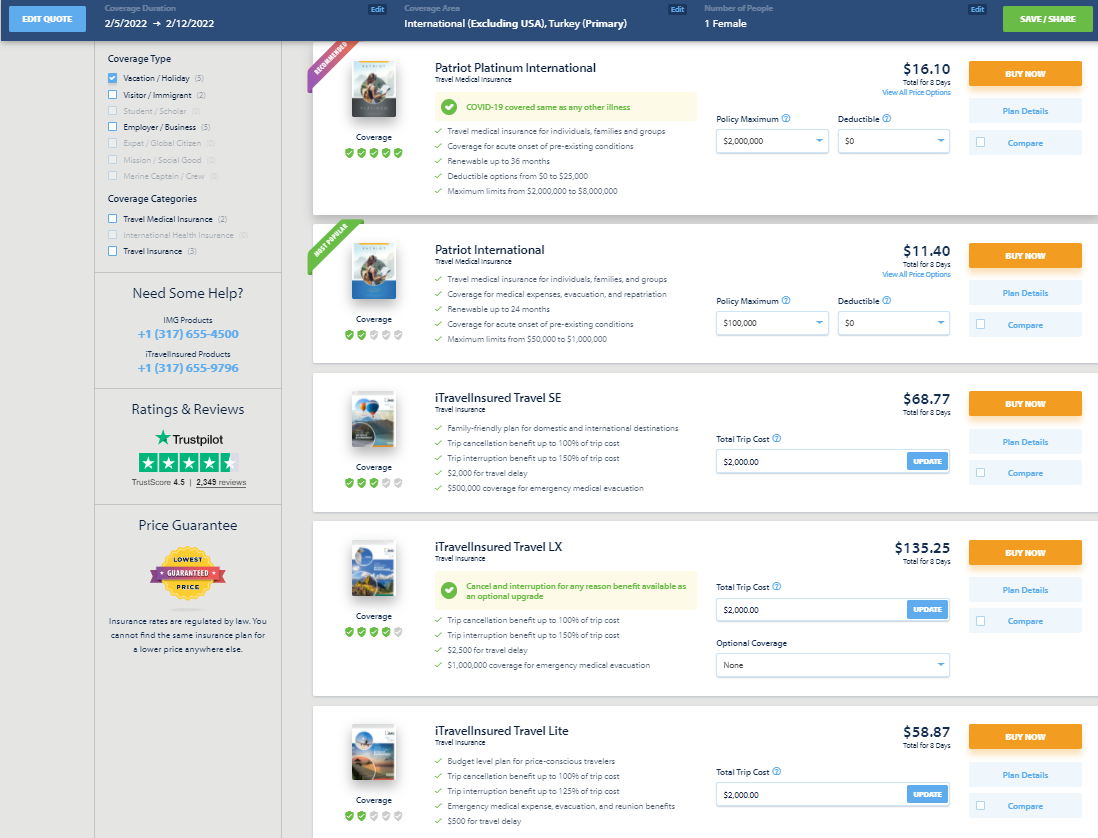

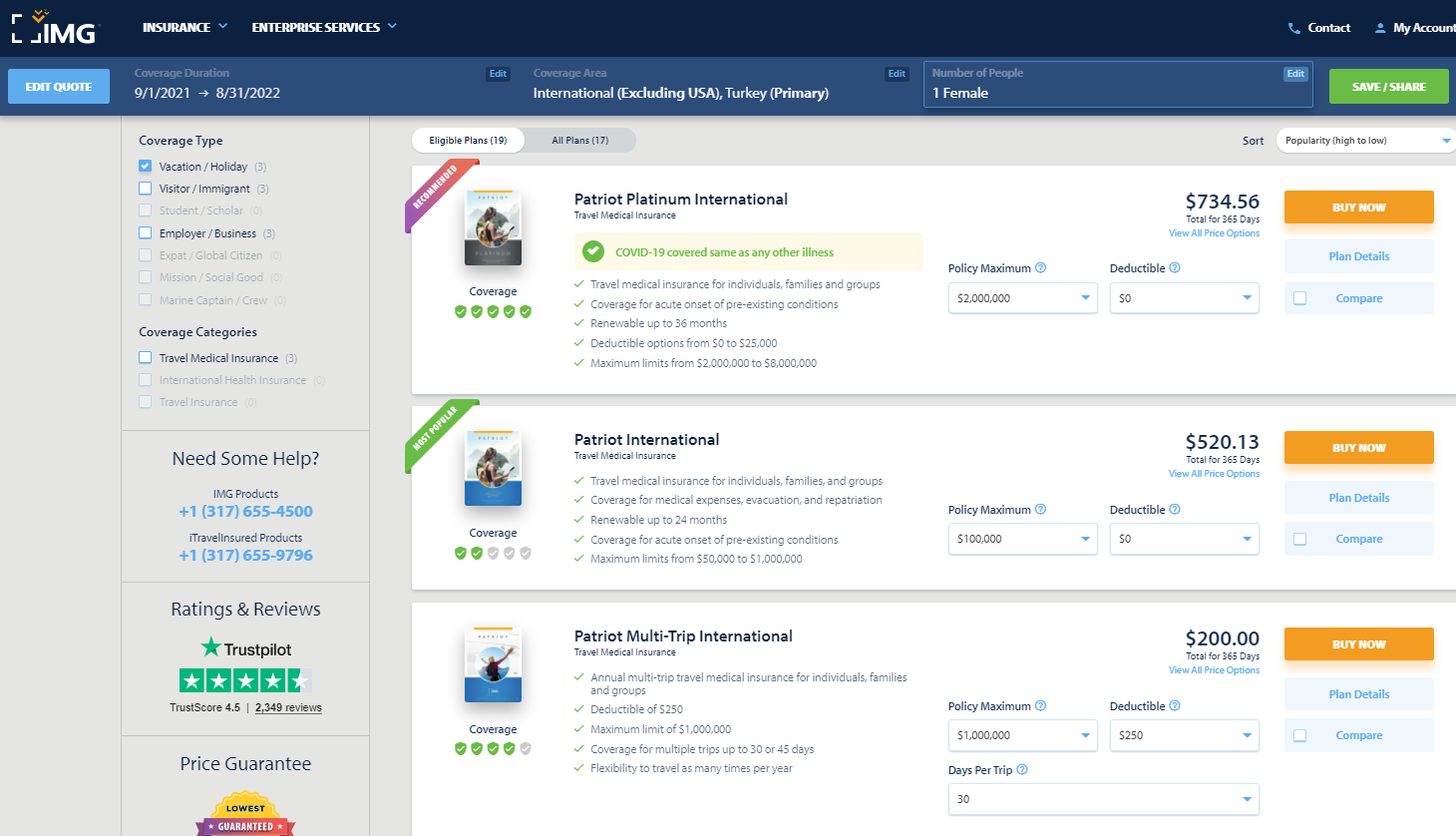

IMG offers various travel medical insurance policies for travelers, as well as comprehensive travel insurance policies. For a single trip of 90 days or less, there are five policy types available for vacation or holiday travelers. Although you must enter your gender, males and females received the same quote for my one-week search.

You can purchase an annual multi-trip travel medical insurance plan. Some only cover trips lasting up to 30 or 45 days, but others provide coverage for longer trips.

See IMG's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Most plans may cover preexisting conditions under set parameters or up to specific amounts. For example, the iTravelInsured Travel LX travel insurance plan shown above may cover preexisting conditions if you purchase the insurance within 24 hours of making the final payment for your trip.

For the travel medical insurance plans shown above, preexisting conditions are covered for travelers younger than 70. However, coverage is capped based on your age and whether you have a primary health insurance policy.

- Some annual multi-trip plans are modestly priced.

- iTravelInsured Travel LX may offer optional cancel for any reason and interruption for any reason coverage, if eligible.

Purchase your policy here: IMG .

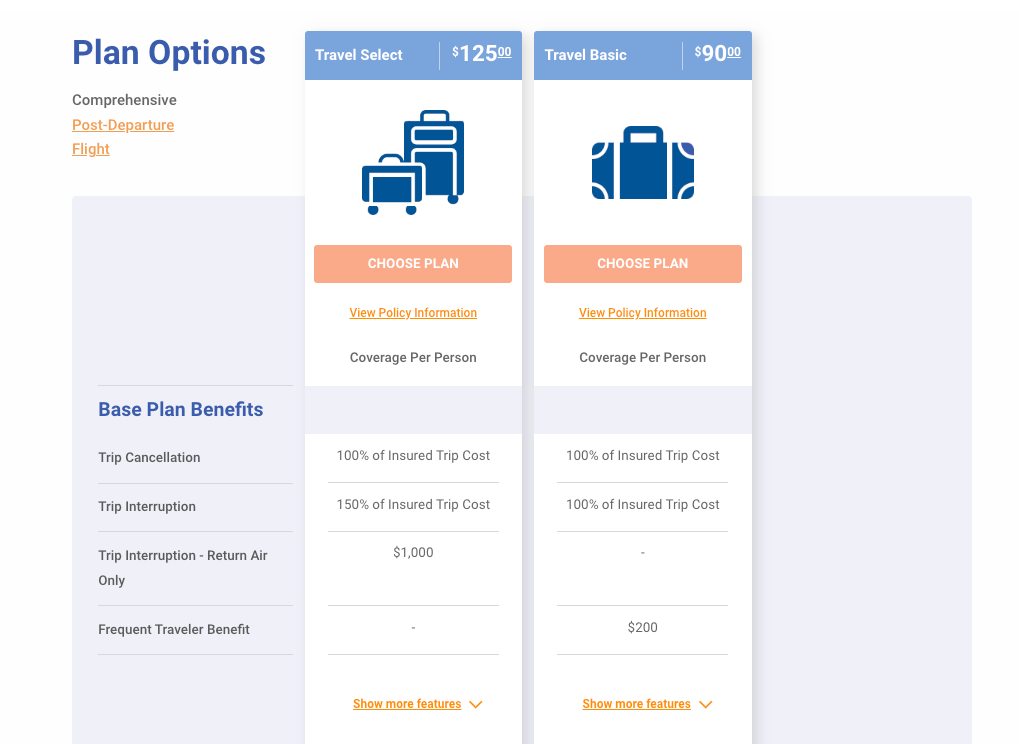

Travelex Insurance

Travelex offers three single-trip plans: Travel Basic, Travel Select and Travel America. However, only the Travel Basic and Travel Select plans would be applicable for my trip to Turkey.

See Travelex's COVID-19 coverage statement for coronavirus-specific information.

Typically, Travelex won't cover losses incurred because of a preexisting medical condition that existed within 60 days of the coverage effective date. However, the Travel Select plan may offer a preexisting condition exclusion waiver. To be eligible for this waiver, the insured traveler must meet all the following conditions:

- You purchase the plan within 15 days of the initial trip payment.

- The amount of coverage purchased equals all prepaid, nonrefundable payments or deposits applicable to the trip at the time of purchase. Additionally, you must insure the costs of any subsequent arrangements added to the same trip within 15 days of payment or deposit.

- All insured individuals are medically able to travel when they pay the plan cost.

- The trip cost does not exceed the maximum trip cost limit under trip cancellation as shown in the schedule per person (only applicable to trip cancellation, interruption and delay).

- Travelex's Travel Select policy can cover trips lasting up to 364 days, which is longer than many single-trip policies.

- Neither Travelex policy requires receipts for trip and baggage delay expenses less than $25.

- For emergency evacuation coverage, you or someone on your behalf must contact Travelex and have Travelex make all transportation arrangements in advance. However, both Travelex policies provide an option if you cannot contact Travelex: Travelex will pay up to what it would have paid if it had made the arrangements.

Purchase your policy here: Travelex Insurance .

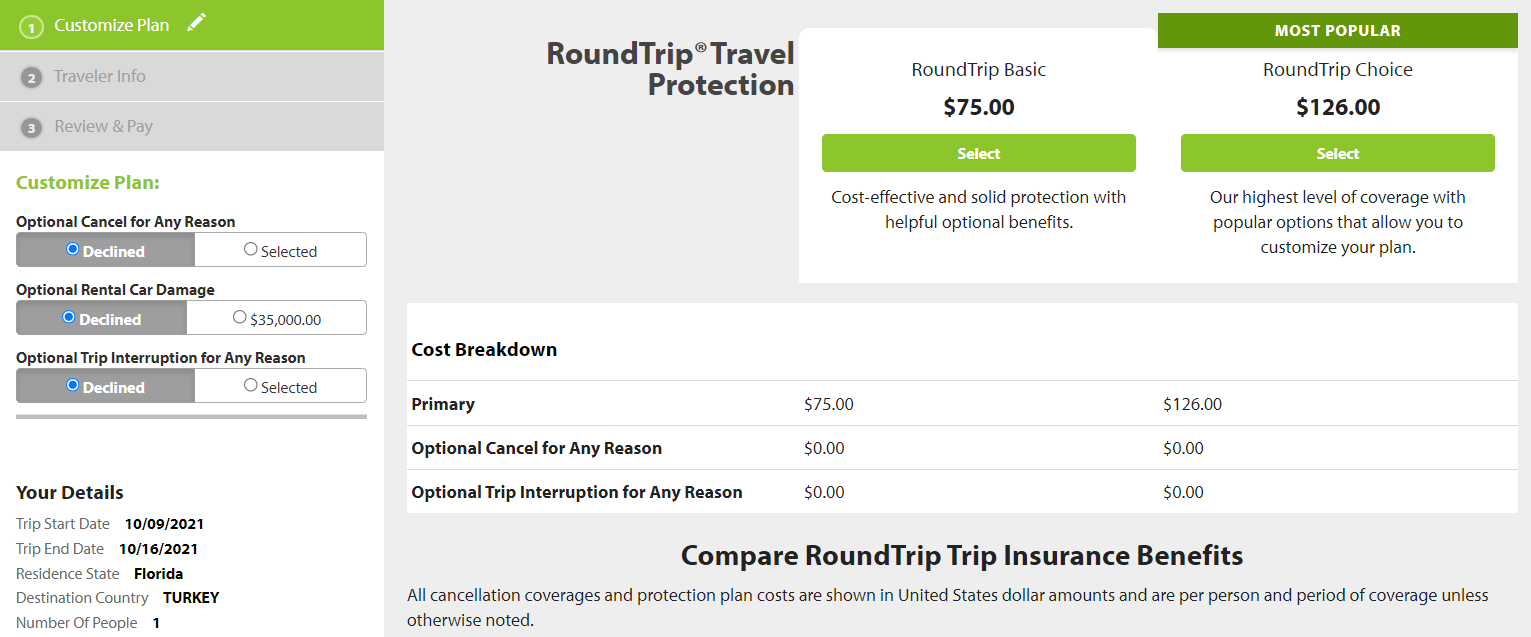

Seven Corners

Seven Corners offers a wide variety of policies. Here are the policies that are most applicable to travelers on a single international trip.

Seven Corners also offers many other types of travel insurance, including an annual multi-trip plan. You can choose coverage for trips of up to 30, 45 or 60 days when purchasing an annual multi-trip plan.

See Seven Corner's page on COVID-19 for additional policy information as it relates to coronavirus-related claims.

Typically, Seven Corners won't cover losses incurred because of a preexisting medical condition. However, the RoundTrip Choice plan offers a preexisting condition exclusion waiver. To be eligible for this waiver, you must meet all of the following conditions:

- You buy this plan within 20 days of making your initial trip payment or deposit.

- You or your travel companion are medically able and not disabled from travel when you pay for this plan or upgrade your plan.

- You update the coverage to include the additional cost of subsequent travel arrangements within 15 days of paying your travel supplier for them.

- Seven Corners offers the ability to purchase optional sports and golf equipment coverage. If purchased, this extra insurance will reimburse you for the cost of renting sports or golf equipment if yours is lost, stolen, damaged or delayed by a common carrier for six or more hours. However, Seven Corners must authorize the expenses in advance.

- You can add cancel for any reason coverage or trip interruption for any reason coverage to RoundTrip plans. Although some other providers offer cancel for any reason coverage, trip interruption for any reason coverage is less common.

- Seven Corners' RoundTrip Choice policy offers a political or security evacuation benefit that will transport you to the nearest safe place or your residence under specific conditions. You can also add optional event ticket registration fee protection to the RoundTrip Choice policy.

Purchase your policy here: Seven Corners .

World Nomads

World Nomads is popular with younger, active travelers because of its flexibility and adventure-activities coverage on the Explorer plan. Unlike many policies offered by other providers, you don't need to estimate prepaid costs when purchasing the insurance to have access to trip interruption and cancellation insurance.

World Nomads offers two single-trip plans.

World Nomads has a page dedicated to coronavirus coverage , so be sure to view it before buying a policy.

World Nomads won't cover losses incurred because of a preexisting medical condition (except emergency evacuation and repatriation of remains) that existed within 90 days of the coverage effective date. Unlike many other providers, World Nomads doesn't offer a waiver.

- World Nomads' policies cover more adventure sports than most providers, so activities such as bungee jumping are included. The Explorer policy covers almost any adventure sport, including skydiving, stunt flying and caving. So, if you partake in adventure sports while traveling, the Explorer policy may be a good fit.

- World Nomads' policies provide nonmedical evacuation coverage for transportation expenses if there is civil or political unrest in the country you are visiting. The coverage may also transport you home if there is an eligible natural disaster or a government expels you.

Purchase your policy here: World Nomads .

Other options for buying travel insurance

This guide details the policies of eight providers with the information available at the time of publication. There are many options when it comes to travel insurance, though. To compare different policies quickly, you can use a travel insurance aggregator like InsureMyTrip to search. Just note that these search engines won't show every policy and every provider, and you should still research the provided policies to ensure the coverage fits your trip and needs.

You can also purchase a plan through various membership associations, such as USAA, AAA or Costco. Typically, these organizations partner with a specific provider, so if you are a member of any of these associations, you may want to compare the policies offered through the organization with other policies to get the best coverage for your trip.

Related: Should you get travel insurance if you have credit card protection?

Is travel insurance worth getting?

Whether you should purchase travel insurance is a personal decision. Suppose you use a credit card that provides travel insurance for most of your expenses and have medical insurance that provides adequate coverage abroad. In that case, you may be covered enough on most trips to forgo purchasing travel insurance.

However, suppose your medical insurance won't cover you at your destination and you can't comfortably cover a sizable medical evacuation bill or last-minute flight home . In that case, you should consider purchasing travel insurance. If you travel frequently, buying an annual multi-trip policy may be worth it.

What is the best COVID-19 travel insurance?

There are various aspects to keep in mind in the age of COVID-19. Consider booking travel plans that are fully refundable or have modest change or cancellation fees so you don't need to worry about whether your policy will cover trip cancellation. This is important since many standard comprehensive insurance policies won't reimburse your insured expenses in the event of cancellation if it's related to the fear of traveling due to COVID-19.

However, if you book a nonrefundable trip and want to maintain the ability to get reimbursed (up to 75% of your insured costs) if you choose to cancel, you should consider buying a comprehensive travel insurance policy and then adding optional cancel for any reason protection. Just note that this benefit is time-sensitive and has eligibility requirements, so not all travelers will qualify.

Providers will often require CFAR purchasers insure the entire dollar amount of their travels to receive the coverage. Also, many CFAR policies mandate that you must cancel your plans and notify all travel suppliers at least 48 hours before your scheduled departure.

Likewise, if your primary health insurance won't cover you while on your trip, it's essential to consider whether medical expenses related to COVID-19 treatment are covered. You may also want to consider a MedJet medical transport membership if your trip is to a covered destination for coronavirus-related evacuation.

Ultimately, the best pandemic travel insurance policy will depend on your trip details, travel concerns and your willingness to self-insure. Just be sure to thoroughly read and understand any terms or exclusions before purchasing.

What are the different types of travel insurance?

Whether you purchase a comprehensive travel insurance policy or rely on the protections offered by select credit cards, you may have access to the following types of coverage:

- Baggage delay protection may reimburse for essential items and clothing when a common carrier (such as an airline) fails to deliver your checked bag within a set time of your arrival at a destination. Typically, you may be reimbursed up to a particular amount per incident or per day.

- Lost/damaged baggage protection may provide reimbursement to replace lost or damaged luggage and items inside that luggage. However, valuables and electronics usually have a relatively low maximum benefit.

- Trip delay reimbursement may provide reimbursement for necessary items, food, lodging and sometimes transportation when you're delayed for a substantial time while traveling on a common carrier such as an airline. This insurance may be beneficial if weather issues (or other covered reasons for which the airline usually won't provide compensation) delay you.

- Trip cancellation and interruption protection may provide reimbursement if you need to cancel or interrupt your trip for a covered reason, such as a death in your family or jury duty.

- Medical evacuation insurance can arrange and pay for medical evacuation if deemed necessary by the insurance provider and a medical professional. This coverage can be particularly valuable if you're traveling to a region with subpar medical facilities.

- Travel accident insurance may provide a payment to you or your beneficiary in the case of your death or dismemberment.

- Emergency medical insurance may provide payment or reimburse you if you must seek medical care while traveling. Some plans only cover emergency medical care, but some also cover other types of medical care. You may need to pay a deductible or copay.

- Rental car coverage may provide a collision damage waiver when renting a car. This waiver may reimburse for collision damage or theft up to a set amount. Some policies also cover loss-of-use charges assessed by the rental company and towing charges to take the vehicle to the nearest qualified repair facility. You generally need to decline the rental company's collision damage waiver or similar provision to be covered.

Should I buy travel health insurance?

If you purchase travel with credit cards that provide various trip protections, you may not see much need for additional travel insurance. However, you may still wonder whether you should buy travel medical insurance.

If your primary health insurance covers you on your trip, you may not need travel health insurance. Your domestic policy may not cover you outside the U.S., though, so it's worth calling the number on your health insurance card if you have coverage questions. If your primary health insurance wouldn't cover you, it's likely worth purchasing travel medical insurance. After all, as you can see above, travel medical insurance is often very modestly priced.

How much does travel insurance cost?

Travel insurance costs depend on various factors, including the provider, the type of coverage, your trip cost, your destination, your age, your residency and how many travelers you want to insure. That said, a standard travel insurance plan will generally set you back somewhere between 4% and 10% of your total trip cost. However, this can get lower for more basic protections or become even higher if you include add-ons like cancel for any reason protection.

The best way to determine how much travel insurance will cost is to price out your trip with a few providers discussed in the guide. Or, visit an insurance aggregator like InsureMyTrip to quickly compare options across multiple providers.

When and how to get travel insurance

For the most robust selection of available travel insurance benefits — including time-sensitive add-ons like CFAR protection and waivers of preexisting conditions for eligible travelers — you should ideally purchase travel insurance on the same day you make your first payment toward your trip.

However, many plans may still offer a preexisting conditions waiver for those who qualify if you buy your travel insurance within 14 to 21 days of your first trip expense or deposit (this time frame may vary by provider). If you don't need a preexisting conditions waiver or aren't interested in CFAR coverage, you can purchase travel insurance once your departure date nears.

You must purchase coverage before it's needed. Some travel medical plans are available for purchase after you have departed, but comprehensive plans that include medical coverage must be purchased before departing.

Additionally, you can't buy any medical coverage once you require medical attention. The same applies to all travel insurance coverage. Once you recognize the need, it's too late to protect your trip.

Once you've shopped around and decided upon the best travel insurance plan for your trip, you should be able to complete your purchase online. You'll usually be able to download your insurance card and the complete policy shortly after the transaction is complete.

Related: 7 times your credit card's travel insurance might not cover you

Bottom line

Not all travel insurance policies and providers are equal. Before buying a plan, read and understand the policy documents. By doing so, you can choose a plan that's appropriate for you and your trip — including the features that matter most to you.

For example, if you plan to go skiing or rock climbing, make sure the policy you buy doesn't contain exclusions for these activities. Likewise, if you're making two back-to-back trips during which you'll be returning home for a short time in between, be sure the plan doesn't terminate coverage at the end of your first trip.

If you're looking to cover a sudden recurrence of a preexisting condition, select a policy with a preexisting condition waiver and fulfill the requirements for the waiver. After all, buying insurance won't help if your policy doesn't cover your losses.

Disclaimer : This information is provided by IMT Services, LLC ( InsureMyTrip.com ), a licensed insurance producer (NPN: 5119217) and a member of the Tokio Marine HCC group of companies. IMT's services are only available in states where it is licensed to do business and the products provided through InsureMyTrip.com may not be available in all states. All insurance products are governed by the terms in the applicable insurance policy, and all related decisions (such as approval for coverage, premiums, commissions and fees) and policy obligations are the sole responsibility of the underwriting insurer. The information on this site does not create or modify any insurance policy terms in any way. For more information, please visit www.insuremytrip.com .

- Share full article

Advertisement

Travel Insurance: What It Covers and When to Buy It

By Elaine Glusac

In the wake of Covid, travel insurance sales have spiked with the rebound in travel as people seek to protect their investments against flight delays and cancellations, extreme weather events and the persistence of the virus. But travel insurance is complicated with a range of benefits, inclusions and prices. Here’s what you need to know before you buy.

Know what’s covered

Generally speaking, travel insurance covers unforeseen events, like an illness in the family, the loss of a job or a natural disaster, that force you to cancel or interrupt a trip. It can also apply in the event of a strike at a transportation company, a terrorist attack in your destination or when your travel provider goes bankrupt. These are known as covered reasons . Most polices also include medical coverage, which is useful abroad where your health insurance may not cover you.

While policy prices vary based on age, length of travel and type of coverage, expect to pay between 4 to 10 percent of your entire trip cost to get insured.

Insure nonrefundable expenses

Travel insurance was designed to protect expenses you can’t get back any other way when things go wrong. Think of nonrefundable Airbnb reservations or the cost of a cruise to the Galápagos.

If your hotel is refundable and you can get the value of your flights back in credits, you can skip travel insurance.

Buy close to booking

Travel insurers say the best time to buy travel insurance — which usually takes effect within a day of purchase — is just after making your travel plans to have the largest possible coverage window. A lot can happen between booking a Christmas market cruise in Europe in June and going in December.

With many plans, purchasing travel insurance 10 to 14 days from your first trip payment entitles you to “early purchase” benefits such as a waiver for pre-existing medical conditions that impact travel. If such a waiver is included, it is usually prominent in a summary of benefits, so read it carefully.

“Not all plans have a pre-existing condition waiver,” said Suzanne Morrow, the senior vice president of InsureMyTrip.com , an online insurance marketplace. “If I have a heart condition and if something occurs, I don’t want it excluded, so I would need to buy a policy within 14 days of the first dollar spent.”

Hedge against the weather

You can’t control the weather, but you can insure against its unexpected disruptions. For example, if you’re ready to jump on great rates in the Caribbean during the height of hurricane season, buy your insurance immediately after booking so that if a hurricane develops and your destination is evacuated, you’ll be covered.

“That’s probably the biggest use case for travel insurance,” said Stan Sandberg, a co-founder of TravelInsurance.com , an online marketplace. He counsels travelers to buy early — if you wait and the storm is named it will be too late to insure against it, because it is no longer an unforeseen event.

Similarly, with winter travel, if you’ve purchased nonrefundable ski lift tickets and a storm prevents you from reaching the resort, you may be able to claim the unused portion of your ski pass.

This coverage may prove more valuable as climate change exacerbates weather events like hurricanes and tornadoes, which are considered “natural disasters” and are covered by most policies.

Pick up the phone

With the proliferation of automated insurance offers when you buy airline tickets or tours, travel insurance can feel like a one-size-fits-all product. It is not. Many policies, for example, exclude extreme sports like skydiving and mountain climbing, though there are specialty policies that include them.

If you have a specific concern — a family member is sick or you’re going heli-skiing — the best way to know if a travel insurance policy will cover you is to call an insurer or the help line at a travel insurance marketplace to get advice.

“Tell them the what-if scenario and then you can get professional and accurate advice,” Ms. Morrow said. “Thinking you’re covered and then having your claim denied is salt in the wound.”

Travel insurance does not cover ‘unpleasantries’

What if you’re dreading spending a week in an un-air-conditioned rental in England during a heat wave and decide you don’t want to go? Most standard travel insurance will not cover a change of heart.

“Travel insurance doesn’t cover you for unpleasantries,” said Carol Mueller, the vice president for strategic marketing at Berkshire Hathaway Travel Protection.

A policy upgrade, Cancel for Any Reason coverage, which is not available in every state, will cover a change of heart, usually up until a few days before departure. Most only reimburse 50 to 75 percent of your costs and the purchase must be made within weeks of your initial trip payment. It will bump your insurance premium up 40 to 50 percent, according to the insurance marketplace Squaremouth.com , which only recommends C.F.A.R. for travelers with specific concerns not included under covered reasons for trip cancellation.

A relatively new twist in trip protection, Interruption for Any Reason , works like C.F.A.R. in that it reimburses a portion of your expenses and can be invoked if you decide to bail while you’re on a trip for a reason that isn’t covered by standard trip insurance. Normally, you must buy it within weeks of your initial trip payment and be 72 hours into a trip before you can use it.

Keep records

If something goes wrong and you need to make a claim, you’ll need proof in the form of a paper trail. That could be receipts for clothing you purchased when your bags went missing, a hotel room required when your flight was canceled (along with flight cancellation notices from the airline) or a doctor’s note stating that you have Covid — or another illness — and are unable to travel. (With Covid, a positive test taken at home is not considered official documentation for the purposes of a claim.)

Resist pressure to buy flight insurance

When purchasing an airline ticket online, most carriers offer travel insurance to cover the cost with some version of vaguely menacing language like, “Do you really want to risk your investment?” when you decline.

Don’t fall for it. You may want to insure that ticket, but price out the policy elsewhere. A recent offer to insure a $428 flight for nearly $28 on an airline website cost $12 to $96 with a range of options at InsureMyTrip.com.

The $12 option was closest to the airline’s offer. Caveat emptor.

An earlier version of this article misspelled the first name of the senior vice president of InsureMyTrip.com , an online insurance marketplace. It is Suzanne Morrow, not Suzanna.

How we handle corrections

Open Up Your World

Considering a trip, or just some armchair traveling here are some ideas..

52 Places: Why do we travel? For food, culture, adventure, natural beauty? Our 2024 list has all those elements, and more .

Mumbai: Spend 36 hours in this fast-changing Indian city by exploring ancient caves, catching a concert in a former textile mill and feasting on mangoes.

Kyoto: The Japanese city’s dry gardens offer spots for quiet contemplation in an increasingly overtouristed destination.

Iceland: The country markets itself as a destination to see the northern lights. But they can be elusive, as one writer recently found .

Texas: Canoeing the Rio Grande near Big Bend National Park can be magical. But as the river dries, it’s getting harder to find where a boat will actually float .

- Best overall

- Best for exotic trips

- Best for trip interruption

- Best for family coverage

- Best for long trips

How we reviewed international travel insurance companies

Best international travel insurance for april 2024.

Affiliate links for the products on this page are from partners that compensate us (see our advertiser disclosure with our list of partners for more details). However, our opinions are our own. See how we rate insurance products to write unbiased product reviews.

If you're planning your next vacation or trip out of the country, be sure to factor in travel insurance. Unexpected medical emergencies when traveling can drain your bank account, especially when you're traveling internationally. The best travel insurance companies for international travel can step in to provide you with peace of mind and financial protection while you're abroad.

Best International Travel Insurance Companies

Best overall: Allianz Travel Insurance

Best for exotic travel: World Nomads Travel Insurance

Best for trip interruption coverage: C&F Travel Insured

Best for families: Travelex Travel Insurance

Best for long-term travel: Seven Corners Travel Insurance

Best overall: Allianz

Allianz Travel Insurance offers the ultimate customizable coverage for international trips, whether you're a frequent jetsetter or an occasional traveler. You can choose from an a la carte of single or multi-trip plans, as well as add-ons, including rental car damage, cancel for any reason (CFAR) , adventure sport, and business travel coverage. And with affordable pricing compared to competitors, Allianz is a budget-friendly choice for your international travel insurance needs.

The icing on the cake is Allyz TraveSmart, Allainz's highly-rated mobile app, which has an average rating of 4.4 out of five stars on the Google Play store across over 2,600 reviews and 4.8 out of five stars from over 22,000 reviews on the Apple app store. So, you can rest easy knowing that you can access your policy and file claims anywhere in the world without a hassle.

Read our Allianz travel insurance review here.

Best for exotic trips: World Nomads

World Nomads Travel Insurance offers coverage for over 150 specific activities, so you can focus on the adventure without worrying about gaps in your coverage.

You can select its budget-friendly standard plan, starting at $79. Or if you're an adrenaline junkie seeking more thrills, you can opt for the World Nomads' Explorer plan for $120, which includes extra sports like skydiving, scuba diving, and heli-skiing. And World Nomads offers 24/7 assistance, so you can confidently travel abroad, knowing that help is just a phone call away.

Read our World Nomads travel insurance review here.

Best for trip interruption: C&F Travel Insured

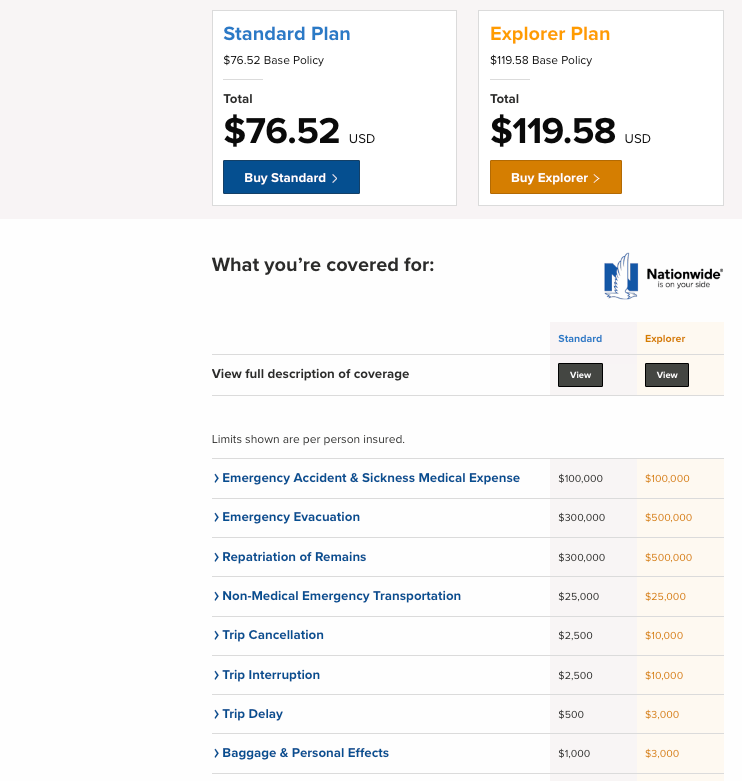

C&F Travel Insured offers 100% coverage for trip cancellation, up to 150% for trip interruption, and reimbursement for up to 75% of your non-refundable travel costs with select plans. This means you don't have to worry about losing your hard-earned money on non-refundable travel costs if your trip ends prematurely.

Travel Insured also stands out for its extensive "reasons for cancellation" coverage. Unlike many insurers, the company covers hurricane warnings from the National Oceanic and Atmospheric Administration (NOAA).

Read our Travel Insured review here.

Best for family coverage: Travelex

Travelex Travel Insurance offers coverage for your whole crew, perfect for when you're planning a family trip. Its family plan insures all your children 17 and under at no additional cost. The travel insurance provider also offers add-ons like adventure sports and car rental collision coverage to protect your family under any circumstance. Got pets? With Travelex's Travel Select plan, you can also get coverage for your furry friend's emergency medical and transportation expenses.

Read our Travelex insurance review here.

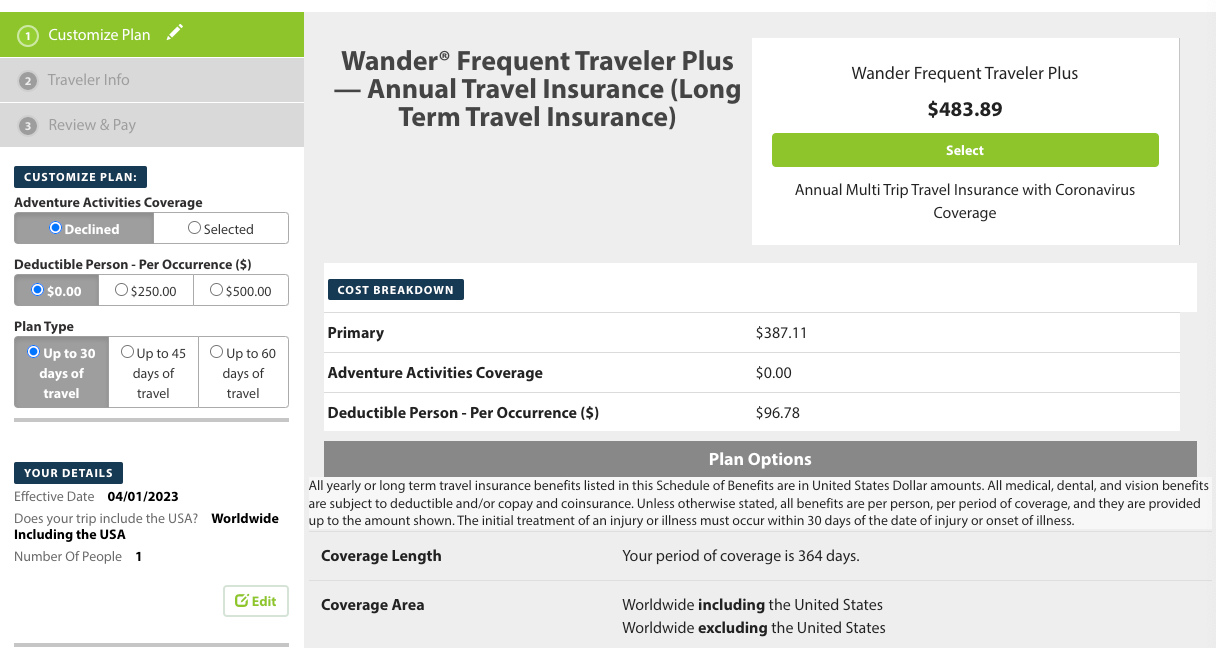

Best for long trips: Seven Corners

Seven Corners Travel Insurance offers specialized coverage that the standard short-term travel insurance policy won't provide, which is helpful if you're embarking on a long-term trip. You can choose from several plans, including the Annual Multi-Trip plan, which provides medical coverage for multiple international trips for up to 364 days. This policy also offers COVID-19 medical and evacuation coverage up to $1 million.

You also get the added benefit of incidental expense coverage. This policy will cover remote health-related services and information, treatment of injury or illness, and live consultations via telecommunication.

Read our Seven Corners travel insurance review here.

How to find the right international travel insurance company

Different travelers and trips require different types of insurance coverage. So, consider these tips if you're in the market to insure your trip.

Determine your needs

- Consider the nature of your travel (leisure, business, or adventure) and the associated risks (medical emergencies, trip cancellations, etc.).

- Determine your budget and the amount of coverage you require.

- Consider the duration of your trip and the countries you'll be visiting, as some policies won't cover specific destinations.

Research the reputation of the company

- Look for the company's reviews and ratings from reputable sources like consumer advocacy groups and independent website reviews.

- Check the provider's financial stability and credit ratings to ensure it can pay out claims reliably.

- Investigate the company's claims process to ensure it can provide timely support if you need to file a claim.

Compare prices

- Get quotes from multiple providers to compare rates and coverage options.

- See if the company provides discounts or special offers to lower your cost.

- Look at the deductible or any out-of-pocket expenses you may have to pay if you file a claim to determine if you can afford it.

Understanding international travel insurance coverage options

Travel insurance can be confusing, but we're here to simplify it for you. We'll break down the industry's jargon to help you understand what travel insurance covers to help you decide what your policy needs. Bear in mind that exclusions and limitations for your age and destination may apply.

Finding the best price for international travel insurance

Your policy cost will depend on several factors, such as the length of your trip, destination, coverage limits, and age. Typically, a comprehensive policy includes travel cancellation coverage costs between 5% and 10% of your total trip cost.

If you're planning an international trip that costs $4,500, you can expect to pay anywhere from $225 to $450 for your policy. Comparing quotes from multiple providers can help you find a budget-friendly travel insurance policy that meets your needs.

We ranked and assigned superlatives to the best travel insurance companies based on our insurance rating methodology . It focuses on several key factors, including:

- Policy types: We analyzed company offerings such as coverage levels, exclusions, and policy upgrades, taking note of providers that offer a range of travel-related issues beyond the standard coverages.

- Affordability: We recognize that cheap premiums don't necessarily equate to sufficient coverage. So, we seek providers that offer competitive rates with comprehensive policies and quality customer service. We also call out any discounts or special offers available.

- Flexibility: Travel insurance isn't one-size-fits-all. We highlight providers that offer a wide array of coverage options, including single-trip, multi-trip, and long-term policies.

- Claims handling: The claims process should be pain-free for policyholders. We seek providers that offer a streamlined process via online claims filing and a track record of handling claims fairly and efficiently.

- Quality customer service: Good customer service is as important as affordability and flexibility. We highlight companies that offer 24/7 assistance and have a strong record of customer service responsiveness.

We consult user feedback and reviews to determine how each company fares in each category. We also check the provider's financial rating and volume of complaints via third-party rating agencies.

The best insurance policy depends on your individual situation, including your destination and budget. However, popular options include Allianz Travel Insurance, World Nomads, and Travel Guard.

International health insurance and travel insurance serve different purposes. While both may cover medical expenses, international health insurance provides long-term health insurance for working abroad. Meanwhile, travel insurance offers short-term coverage for the duration of your trip.

Typically, your regular health insurance won't cover you out of the country, so you'll want to make sure your travel insurance has adequate medical emergency coverage. Depending on your travel plans, you may want to purchase add-ons, such as adventure sports coverage, if you're planning on doing anything adventurous like bungee jumping.

Travel insurance is worth the price for international travel because they're generally more expensive, so you have more to lose. Additionally, your regular health insurance won't cover you in other countries, so without travel insurance, you'll end up paying out of pocket for any emergency medical care you receive out of the US.

- Main content

- Credit cards

- View all credit cards

- Banking guide

- Loans guide

- Insurance guide

- Personal finance

- View all personal finance

- Small business

- Small business guide

- View all taxes

You’re our first priority. Every time.

We believe everyone should be able to make financial decisions with confidence. And while our site doesn’t feature every company or financial product available on the market, we’re proud that the guidance we offer, the information we provide and the tools we create are objective, independent, straightforward — and free.

So how do we make money? Our partners compensate us. This may influence which products we review and write about (and where those products appear on the site), but it in no way affects our recommendations or advice, which are grounded in thousands of hours of research. Our partners cannot pay us to guarantee favorable reviews of their products or services. Here is a list of our partners .

Best Annual Travel Insurance in 2024

Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here's how we make money .

If you’re a frequent traveler, annual travel insurance may be something you’ve been considering. Unlike single-trip insurance, annual travel insurance plans can cover you for an entire year, no matter how often you’re on the road.

Let’s look at the best yearly travel insurance companies, why we choose them and the coverage you can expect.

Factors we considered when picking travel insurance companies

We used the following criteria when choosing which companies we thought were best:

Cost . Annual plans can be expensive — depending on the type of coverage you choose — so we wanted ensure that they stayed affordable.

Types of coverage . Travel insurance for annual travelers can be limited in its coverage. We picked the ones with the broadest range of coverage for possible travel disruptions.

Coverage amounts . Annual trip insurance isn’t worth much if your limits are too low. Instead, we wanted plans with reasonable coverage amounts.

Customizability . If your travels take you to different places, you’ll want the ability to customize your plan. The best annual travel insurance plans can provide this.

» Learn more: What does travel insurance cover?

An overview of the best annual travel insurance

We gathered quotes from various travel insurance companies to determine the best annual travel insurance policies. In these examples, we used a year-long trip by a 22-year-old from Alabama. We indicated the main countries of travel as France and Malaysia, and when asked, put the total trip costs at $6,000.

The average cost for an annual travel insurance plan came out to $220. The plans ranged from $138-$386.

Let’s take a closer look at our top recommendations for annual travel insurance.

1. Allianz Travel

What makes Allianz travel insurance great:

Lower than average cost.

Provides health care and travel insurance benefits.

Includes rental car insurance up to $45,000.

Here’s a snippet from our Allianz Travel insurance review :

“AllTrips Basic (annual plan) is suitable for those who would like emergency medical coverage while abroad but don't need trip cancellation and interruption benefits. The AllTrips Prime, Executive and Premier plans provide an entire year of comprehensive travel insurance benefits.

The Executive and Premier plans offer various levels of trip cancellation and interruption benefits. The Executive plan is specifically designed for business travelers since it offers protection for business equipment.”

2. Seven Corners

What makes Seven Corners great:

Offers up to $20,000 for acute coverage of pre-existing conditions.

Includes up to $1 million for emergency medical evacuation.

Optional add-on for adventure sport activities.

$0 deductible available.

Here’s a snippet from our Seven Corners review :

“Seven Corners offers one annual policy called Travel Medical Annual Multi-Trip. The policy can be customized depending on how long you plan to be away from home for any one trip. You can travel as much as you like during the 364 days, so long as any one trip doesn’t exceed the option selected — 30, 45 or 60 days.”

What makes IMG great:

Good customizability with medical evacuations and sports coverage.

Low $250 deductible.

Includes coverage for semi-private hospital rooms.

Here’s a snippet from our IMG review:

“Some policies provide emergency medical evacuation coverage, while others skip this benefit entirely. This benefit may be more important to you if you travel to a remote location or engage in physical activity such as trekking.

More comprehensive plans may include other benefits such as assistance with acquiring a new passport, reimbursing reward mile redeposit fees or coverage for pre-existing conditions. If these are something you’re interested in, be sure to check that your policy includes these options.”

4. Trawick International

What makes Trawick International great:

100% coverage for trip cancellation and trip interruption.

Emergency medical evacuation included.

Trip delay reimbursement coverage.

Here’s a snippet from our Trawick International review :

“Trawick International is a comprehensive travel insurance provider that offers trip delay and cancellation insurance, baggage delay coverage, medical coverage and medical evacuation, rental car damage protection, and even COVID-19 coverage among its various policies.

Trawick covers trips for worldwide destinations, including for foreign nationals coming to the U.S.”

What does travel insurance cover?

You’ll find a wide variety of coverage types offered by travel insurance policies. This is true whether you're purchasing a single-trip or annual travel insurance plan. Here are some common types you can expect to find:

Accidental death insurance .

Baggage delay and lost luggage insurance .

Cancel for Any Reason insurance .

Emergency evacuation insurance .

Medical insurance .

Rental car insurance .

Trip cancellation insurance .

Trip interruption insurance .

How to choose the best annual travel insurance policy

While we’ve highlighted some of the best annual travel insurance companies, the truth is that the best plan for you isn’t going to be the best plan for someone else. If you’re interested in buying annual travel insurance, you’ll want to collect a variety of quotes to see which policy best fits your needs.

This may mean opting for a plan that covers pre-existing conditions or one that specifically includes high-risk activities. Or, if you’re in a country where health care is notoriously expensive, you may want to choose a policy with higher maximums.

Many credit cards come with complimentary travel insurance .

Whatever the case, do your research first and review all the plan details before making your purchase.

» Learn more: How to find the best travel insurance

If you want to buy annual travel insurance

Annual travel insurance can be a great option if you’re often out of town. With such a wide range of policies available, selecting a plan that fits your needs is easy. We’ve done some of the work for you by choosing the best annual travel insurance companies, all of which made the top of the list for their cost, customizability, types of coverage and plan maximums.

Like any travel insurance policy, the cost of your plan is going to vary. Factors that may affect the cost of your annual travel insurance include your age, where you’re going, how long you’ll be traveling, your policy maximums and whether preexisting conditions are included.

Although not all travel insurance providers offer annual travel insurance, many of them do. We’ve gathered together the five best, including Allianz Travel, World Nomads, Seven Corners, IMG and Trawick International.

How to maximize your rewards

You want a travel credit card that prioritizes what’s important to you. Here are our picks for the best travel credit cards of 2024 , including those best for:

Flexibility, point transfers and a large bonus: Chase Sapphire Preferred® Card

No annual fee: Bank of America® Travel Rewards credit card

Flat-rate travel rewards: Capital One Venture Rewards Credit Card

Bonus travel rewards and high-end perks: Chase Sapphire Reserve®

Luxury perks: The Platinum Card® from American Express

Business travelers: Ink Business Preferred® Credit Card

on Chase's website

1x-10x Earn 5x total points on flights and 10x total points on hotels and car rentals when you purchase travel through Chase Travel℠ immediately after the first $300 is spent on travel purchases annually. Earn 3x points on other travel and dining & 1 point per $1 spent on all other purchases.

60,000 Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That's $900 toward travel when you redeem through Chase Travel℠.

1x-5x 5x on travel purchased through Chase Travel℠, 3x on dining, select streaming services and online groceries, 2x on all other travel purchases, 1x on all other purchases.

60,000 Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That's $750 when you redeem through Chase Travel℠.

1x-2x Earn 2X points on Southwest® purchases. Earn 2X points on local transit and commuting, including rideshare. Earn 2X points on internet, cable, and phone services, and select streaming. Earn 1X points on all other purchases.

50,000 Earn 50,000 bonus points after spending $1,000 on purchases in the first 3 months from account opening.

- Credit Cards

- All Credit Cards

- Find the Credit Card for You

- Best Credit Cards

- Best Rewards Credit Cards

- Best Travel Credit Cards

- Best 0% APR Credit Cards

- Best Balance Transfer Credit Cards

- Best Cash Back Credit Cards

- Best Credit Card Sign-Up Bonuses

- Best Credit Cards to Build Credit

- Best Credit Cards for Online Shopping

- Find the Best Personal Loan for You

- Best Personal Loans

- Best Debt Consolidation Loans

- Best Loans to Refinance Credit Card Debt

- Best Loans with Fast Funding

- Best Small Personal Loans

- Best Large Personal Loans

- Best Personal Loans to Apply Online

- Best Student Loan Refinance

- Best Car Loans

- All Banking

- Find the Savings Account for You

- Best High Yield Savings Accounts

- Best Big Bank Savings Accounts

- Best Big Bank Checking Accounts

- Best No Fee Checking Accounts

- No Overdraft Fee Checking Accounts

- Best Checking Account Bonuses

- Best Money Market Accounts

- Best Credit Unions

- All Mortgages

- Best Mortgages

- Best Mortgages for Small Down Payment

- Best Mortgages for No Down Payment

- Best Mortgages for Average Credit Score

- Best Mortgages No Origination Fee

- Adjustable Rate Mortgages

- Affording a Mortgage

- All Insurance

- Best Life Insurance

- Best Life Insurance for Seniors

- Best Homeowners Insurance

- Best Renters Insurance

- Best Car Insurance

- Best Pet Insurance

- Best Boat Insurance

- Best Motorcycle Insurance

- Travel Insurance

- Event Ticket Insurance

- Small Business

- All Small Business

- Best Small Business Savings Accounts

- Best Small Business Checking Accounts

- Best Credit Cards for Small Business

- Best Small Business Loans

- Best Tax Software for Small Business

- Personal Finance

- All Personal Finance

- Best Budgeting Apps

- Best Expense Tracker Apps

- Best Money Transfer Apps

- Best Resale Apps and Sites

- Buy Now Pay Later (BNPL) Apps

- Best Debt Relief

- Credit Monitoring

- All Credit Monitoring

- Best Credit Monitoring Services

- Best Identity Theft Protection

- How to Boost Your Credit Score

- Best Credit Repair Companies

- Filing For Free

- Best Tax Software

- Best Tax Software for Small Businesses

- Tax Refunds

- Tax Brackets

- Taxes By State

- Tax Payment Plans

- Help for Low Credit Scores

- All Help for Low Credit Scores

- Best Credit Cards for Bad Credit

- Best Personal Loans for Bad Credit

- Best Debt Consolidation Loans for Bad Credit

- Personal Loans if You Don't Have Credit

- Best Credit Cards for Building Credit

- Personal Loans for 580 Credit Score Lower

- Personal Loans for 670 Credit Score or Lower

- Best Mortgages for Bad Credit

- Best Hardship Loans

- All Investing

- Best IRA Accounts

- Best Roth IRA Accounts

- Best Investing Apps

- Best Free Stock Trading Platforms

- Best Robo-Advisors

- Index Funds

- Mutual Funds

- Home & Kitchen

- Gift Guides

- Deals & Sales

- Sign up for the CNBC Select Newsletter

- Subscribe to CNBC PRO

- Privacy Policy

- Your Privacy Choices

- Terms Of Service

- CNBC Sitemap

Follow Select

Our top picks of timely offers from our partners

Is travel insurance worth it?

The right policy can protect your wallet, your belongings and your peace of mind..

Terms apply to American Express benefits and offers. Visit americanexpress.com to learn more.

You might have planned your next vacation, but consider travel insurance before you start packing. A comprehensive policy can protect you if the unexpected happens before or during your trip.

"Travel insurance is often an overlooked investment until the unforeseen happens," says Beth Godlin, president of Aon Affinity Travel Practice . "It's designed to give travelers peace of mind and financial protection against travel risks."

A policy doesn't have to be expensive, according to Godlin, and it can add a layer of protection and security.

Getting travel insurance

How do i get travel insurance, what does travel insurance cover, how much does travel insurance cost.

- Bottom line

There are many options in the travel insurance marketplace: Aggregator site Squaremouth lets you get price quotes from different carriers and, because it receives a commission from the insurance companies on its site, users aren't charged any additional fees.

Allianz has both single-trip and annual plans, with a Cancel For Any Reason (CFAR) policy that reimburses up to 80% of prepaid, non-refundable expenses — more than most similar plans on the market.

In addition to trip cancellation, Allianz's popular OneTrip Prime plan includes travel interruption, emergency medical care and emergency transportation. Children 17 and under are covered for free when traveling with a parent or grandparent.

AIG's Travel Guard® plans are great if you need to customize your coverage: The mid-range Travel Guard Preferred plan pays out 100% for trip cancellation and 150% for trip interruption, with up to $50,000 in coverage for medical expenses and up to $500,000 for emergency evacuation. There's even a payout of up to $1,000 if you miss your connection.

Travel Guard® Travel Insurance

The best way to estimate your costs is to request a quote

Policy highlights

Travel Guard offers a variety of plans to suit travel ranging from road trips to long cruises. For air travelers, Travel Guard can help assist with tracking baggage or covering lost or delayed baggage.

24/7 assistance available

If you're booking a trip with an aggregator site like Expedia , review the details of any travel policy that's offered. Plans are usually based on the elements of the trip (hotel, flight, rental car, etc.) and can differ every time you book.

Travel insurance typically costs between 4 and 10% of the overall price tag for your trip. The cost can vary:

- Plans with higher limits and more optional coverage cost more.

- A plan with a CFAR benefit can cost up to 40% more.

- Older travelers typically pay more because there's more of a likelihood of a claim being filed.

Whichever plan you choose, read the fine print so you understand what you're paying for.

Travel insurance generally covers your expenses, your belongings and your well-being. When shopping for a policy, look for these benefits:

Trip cancellation

If your trip is canceled for a covered reason, a policy will often reimburse airline tickets, hotel rooms, rental cars, tours, cruises and other prepaid, non-refundable expenses. Covered situations can include illness or injury, the death of a family member or traveling companion, job loss, military deployment and even unplanned jury duty, according to Allianz's Daniel Durazo.

Cancellations can also be covered if a natural disaster, severe weather or airline strike prevents your carrier from getting you to your destination for at least 24 hours.

Cancel For Any Reason (CFAR) plans provide a lot more flexibility and typically reimburse 50% to 75% of your expenses. But they can bump up the cost by about 40%, said Durazo, and policyholders are still usually required to cancel no later than 48 hours before their scheduled departure.

Trip delay

Should you experience a hiccup in your plans, your policy can provide some relief: Food, lodging and local transportation are usually covered if a delay is due to severe weather, airline maintenance or civil unrest.

"For a traveler to be eligible, they must be delayed for the minimum amount of time listed on their policy," Squaremouth spokesperson Megan Moncrief said. "Some policies are very lenient and provide benefits for any length delay, while others list a length requirement — usually somewhere between three to 12 hours."

Daily payout limits range from $150 to $250 per traveler, Moncrief said, while the total policy limit can be anywhere from $500 to $2,000. Save any receipts to submit with your reimbursement claim.

Don't miss: The best credit cards with trip delay insurance

Trip interruption

Should you need to cut your trip short due to illness or injury, or if there's a family emergency back home, your policy may reimburse non-refundable expenses you forfeited.

It may also cover the cost of a one-way economy airline ticket home.

Baggage loss

Airlines are required to compensate passengers luggage lost in transit, but a travel insurance policy may have a higher benefit limit, and cover you if your bags, passport or other possessions are lost, damaged or stolen once you've gotten to your destination., The Platinum plan from AXA Assistance USA has a $3,000 benefit limit for lost luggage, well beyond the $1,700 that airlines are required to cover on international flights. AXA has offices in more than 50 countries, with multilingual operators available 24 hours a day to help reschedule flights, book hotels and make other arrangements.

AXA Assistance USA Travel Insurance

AXA Assistance USA offers several travel insurance policies that include travel interruption, trip cancellation, and the option of cancel for any reason (CFAR) coverage.

Travel insurance doesn't cover every loss: Cash is not reimbursable and many policies won't reimburse for expensive jewelry or heirloom items. Read your policy carefully to see what is included.

Medical expenses and emergency evacuation

If you travel within the U.S., your health insurance should cover any illness or injury you sustain. If you're traveling abroad, though, your plan may provide little or no coverage. The right travel insurance should cover doctors' fees and hospital bills, Durazo said.

The provider can also help coordinate care and ensure you're at a medical facility that's up to U.S. standards.

An emergency medical evacuation can be a major expense, costing anywhere from $15,000 to over $200,000, Durazo added.

If you've spent money on nonrefundable airline tickets, tours and hotels, you could be at a loss if something goes awry. Travel insurance covers numerous scenarios, from a medical emergency to a tropical storm. It could be particularly useful if:

- You've spent a lot on prepaid, non-refundable expenses

- You're traveling internationally where your health insurance won't apply

- You're traveling to a remote area

- Your flight involves multiple connections or destinations

"When deciding if travel insurance is right for you, ask yourself how much you could stand to lose if you had to cancel at the last minute," said Godlin.

If you're not as concerned about risk, your credit card may offer built-in travel protection if you book with that card: Chase Sapphire Preferred® , Southwest Rapid Rewards® Plus Card and the *American Express® Gold Card all come with trip cancellation and interruption coverage, among other benefits.

*Eligibility and Benefit level varies by Card. Terms, Conditions and Limitations Apply.

Please visit americanexpress.com/benefitsguide for more details.

Underwritten by New Hampshire Insurance Company, an AIG Company.

Chase Sapphire Reserve®

Earn 5X total points on flights and 10X total points on hotels and car rentals when you purchase travel through Chase Travel℠ immediately after the first $300 is spent on travel purchases annually. Earn 3X points on other travel and dining & 1 point per $1 spent on all other purchases plus, 10X points on Lyft rides through March 2025

Welcome bonus

Earn 60,000 bonus points after you spend $4,000 on purchases in the first 3 months from account opening. That's $900 toward travel when you redeem through Chase Travel℠.

Regular APR

22.49% - 29.49% variable

Balance transfer fee

5%, minimum $5

Foreign transaction fee

Credit needed.

Terms apply.

Read our Chase Sapphire Reserve® review.

Southwest Rapid Rewards® Plus Credit Card

Earn 2X points on Southwest® purchases, 2X points on local transit and commuting, including rideshare; 2X points on internet, cable and phone services; select streaming. 1X points on all other purchases

Earn 50,000 bonus points after spending $1,000 on purchases in the first 3 months from account opening.

21.49% - 28.49% variable

Foreign transaction fees

Excellent/Good

American Express® Gold Card

4X Membership Rewards® points at Restaurants (plus takeout and delivery in the U.S.) and at U.S. supermarkets (on up to $25,000 per calendar year in purchases, then 1X), 3X points on flights booked directly with airlines or on amextravel.com, 1X points on all other purchases

Earn 60,000 Membership Rewards® points after you spend $6,000 on eligible purchases with your new Card within the first 6 months of Card Membership.

Not applicable

See Pay Over Time APR

See rates and fees , terms apply.

Read our American Express® Gold Card review .

Research your card's travel benefits before making any purchases related to your trip.

Policies vary, but most comprehensive travel insurance plans cover travel cancellation and interruption, baggage loss, medical care and emergency transportation.

While the price for coverage varies, most policies cost between 4% and 10% of the trip's prepaid, non-refundable expenses.

When should I get travel insurance?

It's best to take out a policy within days of making your reservations.

Does travel insurance cover COVID-19?

If you contract COVID-19 before or on your trip, it may be covered by your policy's trip cancellation/interruption benefit . You'll likely have to confirm your test results with a diagnosis from a healthcare provider.

Bottom line

Travel can be a wonderful experience, but it involves a lot of time, planning and money. Missing a single connection can have a cascade effect that impacts your flight, hotel room, dinner reservations and more. A good travel insurance policy can provide peace of mind so you can focus on your vacation.

Compare and find the best life insurance

Money matters — so make the most of it. Get expert tips, strategies, news and everything else you need to maximize your money, right to your inbox. Sign up here .

Meet our experts

At CNBC Select, we work with experts with specialized knowledge and authority. For this story, we interviewed Beth Godlin, president of Aon, which provides custom travel insurance for tour operators, cruise lines, travel websites and others. We also spoke with former Squaremouth Megan Moncrief and Allianz communications director Daniel Durazo.

Why trust CNBC Select?

At CNBC Select, our mission is to provide our readers with high-quality service journalism and comprehensive consumer advice so they can make informed decisions with their money. Every insurance article is based on rigorous reporting by our team of expert writers and editors . While CNBC Select earns a commission from affiliate partners on many offers and links, we create all our content without input from our commercial team or any outside third parties, and we pride ourselves on our journalistic standards and ethics.

Catch up on CNBC Select's in-depth coverage of credit cards , banking and money , and follow us on TikTok , Facebook , Instagram and Twitter to stay up to date.

For rates and fees for the American Express® Gold Card , click here .

- Best sole proprietorship business credit cards Jason Stauffer

- This is the best budgeting app to help investors track their money Jasmin Suknanan

- 5 best credit cards with pre-approval or pre-qualification Jason Stauffer

Atlas & Boots

The UK's most popular outdoor travel blog

10 tips for buying annual travel insurance

A comprehensive guide to buying annual travel insurance including what to look out for, the pitfalls to avoid and the questions to ask

Back in 2014, British adrenaline junkie Ben Cornick jumped out of a plane in Fiji at 12,000 feet. There was no way to know at the moment he leapt out of the aircraft that his parachute wouldn’t work properly and that he would plummet to Earth, breaking his leg in three places and shattering his elbow.

It gets worse: Ben hadn’t bought travel insurance and had to pay £20,000 upfront for treatment to save his leg. His parents pulled together their life savings and readied to sell their house.

But then there was an unlikely twist: following media coverage of Ben’s predicament, complete strangers donated money to pay his medical bills, massively reducing the cost to his parents. Thankfully, this case has a happy ending, but we dare say we wouldn’t all be so lucky.

The purpose of this story isn’t to scaremonger; it’s to illustrate that accidents can happen even if, like Ben and skydiving, you have done something a thousand times with no injury. The answer to ‘should I get travel insurance?’ is yes – doubly so if you’re going on a long-term trip. Here’s what to bear in mind when buying annual travel insurance.

1. Start saving early

Annual travel insurance for our round-the-world trip cost £400 for two people, a hefty amount given that we were scrimping and saving for a year to make the trip happen. We bought our insurance very close to our departure date which meant the price tag seriously stung.

To avoid this pain, factor in the cost as early as possible and start saving immediately. This way, you won’t be tempted to forego it altogether.

2. Don’t automatically opt for the cheapest package

It’s tempting, we know. On our past travels, we were covered under the cheapest annual policy. With an entire year of continuous travel ahead of us including lots of outdoor activities, however, we wanted to make sure we would be covered adequately. Needless to say, the cheapest option didn’t quite cut it.

We spent a long time checking individual websites aimed at independent travellers. Eventually, we opted for a more expensive policy, which paid off when we broke our GoPro on a dive in Tonga.

Any good policy should cover accidental loss and damage, as well as medical expenses of £2m for Europe and £5m worldwide. Cancellation should be around £3,000 or at least the cost of the holiday, and personal liability should be around £1m or more.

3. Be aware of date restrictions

Make sure you understand any restrictions and conditions around the dates of your policy. Be particularly aware of the following.

- Most policies won’t cover you if you have already started your trip, so buy before you go.

- If your policy starts when you leave for your trip in say May and you buy your policy in January, will you be covered if your trip is cancelled in February? Many companies don’t make this clear so make sure you ask explicitly.

- If you are backpacking long-term, make sure your policy covers one long period of continuous travel, not multiple short trips.

- If you buy annual travel insurance for one big trip, make sure it remains valid if you go home for a short while and then restart your travels. Some policies stop when you get home, but this isn’t always made clear.

4. Don’t buy from your tour company or cruise line

If you’re booking via a travel agency or tour company, don’t be tempted to buy their own travel insurance. If the company finds itself in financial trouble (e.g. bankruptcy), you may find that you are no longer covered. Buy from a dedicated insurer instead.

5. Ensure it covers the basics

Basic insurance should cover trip cancellation and curtailment, medical emergency, baggage, and flights – and of course, apply to the country or countries you will be visiting. You may also need to consider the following:

- Emergency evacuation: This is sensible if you’re going hiking, mountaineering or staying somewhere isolated.

- Medical repatriation: Many policies offer medical treatment but not transport back to your home.

- Winter or extreme sports: Even if your policy covers winter sports, double-check your specific needs. Some policies won’t cover off-piste skiing at all or will limit your total number of ski days. Others may specify that you need to take a guide on your climbing expeditions.

- Scheduled airline failure: If your airline goes bust, insurance will only cover the costs if your policy covers “scheduled airline failure”, so check for this.

6. Avoid the following pitfalls

- Excess: Does your excess (the amount you have to pay towards a claim) pertain to each claim or each section of your policy? The former means you only pay it once per claim. The latter could mean that if your bag gets stolen with some jewellery, a wallet and a phone in it, you may have to pay the excess three times if those items are in different sections on your policy.

- Caps on losses: Be aware that there are often caps on losses, particularly on electronic items. This means that if you lose a £1,000 laptop but the cap on electronics is £500, the maximum you will receive is £500. If necessary, look into specialist coverage for your electronics.

- Special circumstances around travelling with children: If you are travelling with kids, be aware that many policies don’t cover them if they don’t live with you (i.e. if you are divorced or separated and live somewhere else). Double-check this if applicable.

7. Be aware of exemptions

As you may expect, there are several exemptions which may result in the rejection of your claim. Be aware of the following.

- Cruises: Many annual travel insurance policies don’t include cruises so do check this if you think you might end up on one ( like we did! ).

- Alcohol/drugs: Policies do not usually cover alcohol- or drug-related incidents so be careful.

- Unstated pre-existing medical conditions: If you haven’t been completely upfront about any/all your pre-existing medical conditions, you could nullify your entire policy. This includes minor ailments like asthma. If in doubt, ask the insurer.

- Specific locations: Obviously, you need to check that your policy covers every country you will be visiting. Make sure you double-check that you’re covered any time you decide to go to an unplanned country just in case it will void your coverage.

- Reckless behaviour: If an incident happened as a result of your reckless behaviour, you could find yourself out of pocket. There is no objective definition of “reckless” behaviour but, in essence, it’s something a reasonable person would not partake in. (I’m not sure if sitting on the rim of an active volcano counts or not…)

8. Have a look at the claims process

Before you book your annual travel insurance policy, have a look at the claims process. Can it be filed online? Is it relatively straightforward or does it involve multiple long-distance phone calls? (On this note: make sure you keep your receipts.)

Finally, if you are a victim of a crime, make sure you go through official legal procedures (file a complaint and obtain a crime reference number). In essence, the more paperwork you have to support your claim, the better chance you’ll have of being reimbursed.

9. Check Trustpilot ratings